Nigeria’s Brent crude oil is selling at $63 while the government’s benchmark for oil in the 2021 budget is pegged at $40. This means the Excess Crude Account (ECA) will have more dollars in its coffers. Unlike 2020, when the benchmark had to be reversed from $57 to $30 at the height of the COVID-19 outbreak when global oil prices were as low as $20, things look a bit better for the country right now.

The price of oil influences the dollar to Naira exchange rate. When oil price increases, Nigeria has more dollars to fund its deficit national budget and execute projects, but when price crashes, the Central Bank of Nigeria (CBN) begins to seek means to accrue more funds to the government, often including devaluation of the Naira.

Source: OilPrice.com

The apex bank has a long-documented history of banning or tagging legal imports and transactions as illegal whenever there is a global oil prices crash. In 2020 alone, CBN added fertilizer and agricultural produce imports to the FOREX restriction list and also directed diaspora remittances to be received in foreign currency (US Dollars) through the recipients’ designated bank of choice. They aim these policies at sustaining the official exchange rate of Naira to dollar—the most sought after currency in FX— and increase the supply of dollars within the country.

But CBN conveniently forgets that capping official FX rate is counterproductive—as Interbank, Bureau de Change, and wire rates determine the prevailing FX rate—when it puts restrictions on access to the foreign currencies.

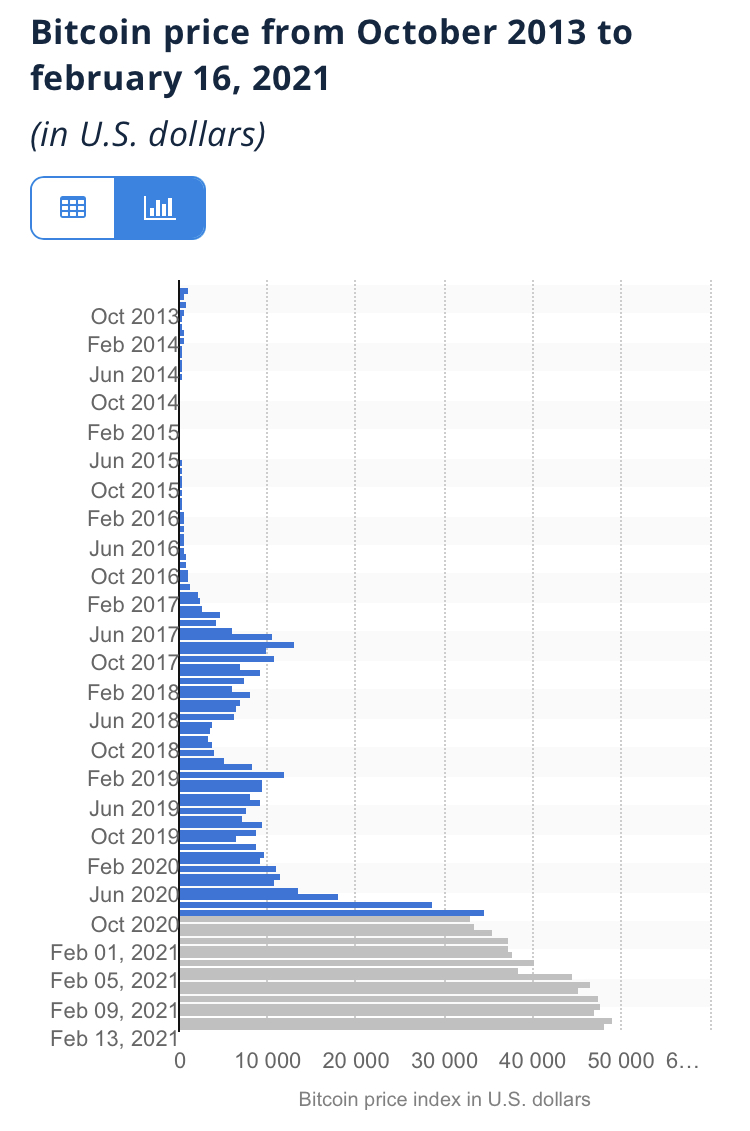

Then comes cryptocurrency, a digital currency which is not subject to exchange rate depreciation, oil price fluctuations, inflation and capital control. Though launched in 2009, Cryptocurrency only gained traction in Nigeria around 2017. The meteoric rise of crypto, especially Bitcoin which went from $900 in January 2017 to over $20,000 in the same year, peaked Nigerians’ interest in digital currencies as a new medium for investment, e-commerce. Though, the CBN warned banks and Nigerians that crypto was not safe and volatile.

Source: Statista

BuyCoins estimates in 2020 revealed that the total volume of bitcoin traded in Nigeria stood at $200 million per month, this is more than the trades on the Nigerian Stock Exchange (NSE)—$131 million in Q2 of 2020. In the same year, the Securities and Exchange Commission (SEC) recognised the validity of cryptocurrency as investments and made rules to regulate what it termed, Virtual Financial Assets.

Also, there were reports that Feminist Coalition—a non-profit activist group received over $80,000 worth of BTC in donations during the #EndSARS peaceful protest in October. Between 2015 to 2020, we have traded more than $566 million worth of bitcoin in Nigeria, making it the first in Africa and second largest Bitcoin market in the world, after the U.S.

This is the reason it outraged Nigerians when CBN issued a circular on February 5, 2020 prohibiting commercial banks and other financial institutions from dealing in cryptocurrency or facilitating payments related to it. The outrage turned to deep contempt as the apex bank also directed these financial institutions to identify customers that have used their systems to perform crypto-related transactions and close it immediately.

CBN’s prohibition of the use of Naira and Nigerian financial institutions as middlemen in crypto trading is quite harmful to Nigeria’s ecosystem and economy, taking into cognisance that the fluctuating global oil price exposes the naira to financial volatility, made worse by CBN’s stringent rules to curtail demand for foreign currencies like dollars which pushes the supply overboard and scarcity of these currencies lead to a rise in its naira equivalent, especially in the black market.

Not only that, the prohibition setback Africa’s crypto market, which Nigeria leads. It will also cripple Nigerians’ Fintech ecosystem, especially platforms like BuyCoins, Patricia, and Quidax that were setup to make crypto trading and investment easier for Nigerians.

Without a doubt, the ban will have a negative effect on the ability of Nigerians to flourish and prosper. It will put an end to the employment opportunities inherent in Nigeria’s crypto trading, confiscate Nigerian importers’ alternate payment system for international trade, and increase the risk of fraud during the source for FX through the black market.

In Africa, regulators have a penchant for banning what they do not understand, take Algeria, Ghana, Kenya, Libya and Morocco, and Libya as examples. However, Nigeria should take a cue from Rwanda and South Africa, as prohibiting cryptocurrencies will not be enough to create an economic balance for its multiple sectors, improve its financial market or boost the value of naira.

Inevitably, crypto restrictions have opened up Nigerian market to innovative scrambles, and rather than CBN sinking the financial systems further, it would be beneficial to Nigeria’s economy to accept, regulate and restructure crypto as a failsafe digital currency devoid of the highlighted ills which made the apex bank restrict it.

This article conveys the views of the author and not necessarily that of Ominira Initiative.