On December 31, 2020, President Muhammadu Buhari signed the Finance Bill 2020 into law and it became effective at the start of the year 2021. The Finance Act, a culmination of amendments to tax and fiscal legislations was aimed at improving the ease of doing business in Nigeria, especially for investors and small and medium scale enterprises (SMEs).

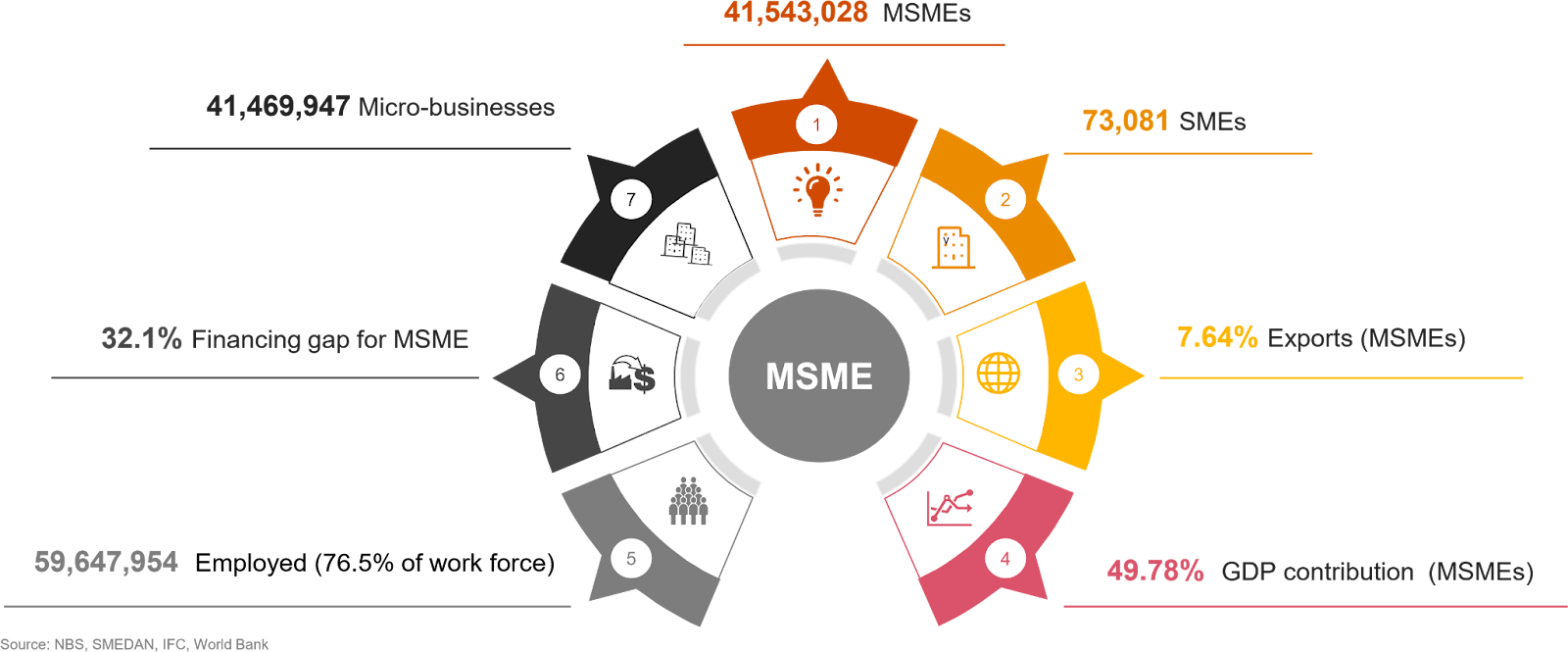

In Africa’s most populous country, SMEs account for 96% of businesses in the country while contributing about 50% to the national GDP, according to PWC 2020 MSME Survey. These SMEs are mainly sole proprietorships business and private limited liability companies.

Despite the several addendums in the finance act which redefines the composition of a small company, its financial strength, restructures tax returns while granting them tax exemptions and holidays as incentives, not to forget the priority status bestowed on SMEs in the Companies and Allied Matters Act (CAMA) 2020, they [small businesses] are still caught in the web of forward and backward linkages from regulatory policies enacted by the same government.

The Central Bank of Nigeria (CBN), as a regulatory body, is always lurking at the corners of every monetary and financial policy, these past few months it has become quite brutal at issuing regulations which affects the growth and survival of small companies.

In 2018, the CBN instigated the recapitalization of microfinance banks (MFBs), stating that tier 1 unit MFBs must meet N100 million capital threshold by April 2020 and crossover to N200 million by April 2021 while Tier 2 unit MFBs should meet a N35 million capital threshold by April 2020 and increase it to N150 million by April 2021.

MFBs which are mostly SMEs due to their capital base were put on a pressure cooker by the apex bank. However, due to the COVID-19 pandemic, the deadline was extended to 2022 before the House of Representative intervened which led to suspension of the policy. Nonetheless, this policy is harmful to SMEs striving to grow their customer base and keep business afloat, especially Fintechs companies which fall within these categories of business.

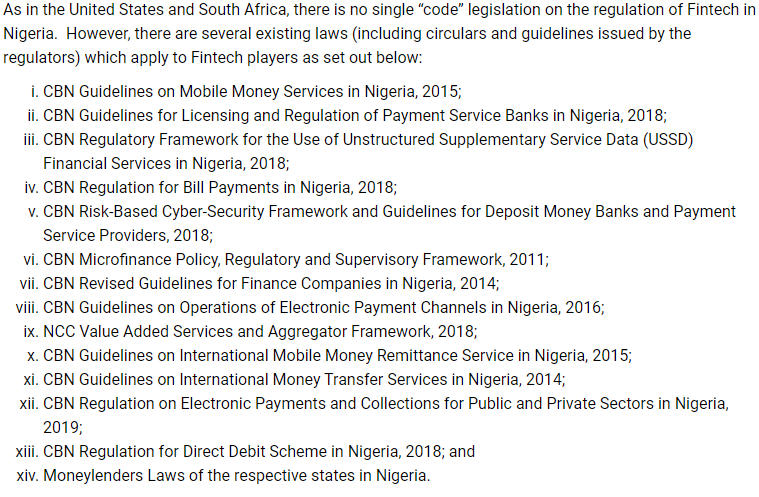

Global Legal Insights pointed out that within the past six years, the CBN has fourteen guidelines and regulations which are in effect for fintech companies in Nigeria, an overkill which affects productivity and makes ease of doing business quite redundant. In 2020 alone, there have been major regulations from the apex ranging from cryptocurrency ban, foreign currency deposit limit to USSD charges.

The Deposit Money Banks (DMBs) have been restricted from engaging in any crypto transaction, a move that puts the economy at a financial volatility judging by the fluctuation of global oil prices and depreciating value of naira, which affects all businesses in Nigeria. Also, at a time when Nigeria is still transitioning to cashless transactions and economy, the CBN has capped the monthly deposit limit of foreign currency into accounts, a move that could affect service delivery and e-commerce businesses.

SMEs employ 76.5 percent of Nigeria’s workforce and everytime there is financial regulation that affects these businesses, it threatens job security and strains the unemployment rate in the country. Not only that, a sector that contributes about 50 percent to the nation’s GDP still has more to offer.

Cryptocurrency trade is creating new employment opportunities for entrepreneurs and investors that will add value to Nigeria’s economy. Recapitalisation of MFBs will restrict investors from dabbling into other untapped areas of Fintech; so, removing certain financial regulations will usher in a new wave for ease of business especially for small businesses, supported by CAMA 2020 and Finance Act 2020. This will help them break even and transition to other business types without having to worry about stringent regulations. Also, these regulations affect e-commerce services, a major part of small businesses in Nigeria from growing into a multimillion dollar sector.

Nigerian Government and its regulatory agencies have an incurable habit for banning and restricting financial innovations and this is quite detrimental to the country’s growth and development, as globalisation has made it clear that only countries that have digitised its numerous sectors can thrive and prosper.